The Cash Flow Statement

This is the third installment of our posts regarding help with understanding Financial Statements: the Cash Flow Statement.

The title itself basically defines what is in the Cash Flow Statement, cash and how it flows through a company. The Cash Flow Statement is one of the most important statements of the three Financial Statements as positive Cash Flow is good and negative cash flow can be considered bad. A company’s cash flow does not always have to be positive to indicate financial health as there will be times a company will spend more than they make intentionally. A simple example would be a company growing rapidly and cash requirements to increase inventory to fulfill orders may be larger than the money being received at the same time from current sales.However, this can be a slippery slope as sustained negative cash flow can put a company out of business.

The Cash Flow Statement is be derived from the Balance Sheet and the Income Statement of the Financial Statements. Cash Flow Statements can be monthly, quarterly, and annually. In my experience a company needs to watch all three Financial Statements monthly and report them to their stakeholders quarterly or annually.

There are three parts to the cash flow statement, Operating Cash Flow, Investing Cash Flow, and Financing Cash Flow. They are distinct in what they tell you and they are added together to give you a complete picture of the total cash flow.

The Operating Cash Flow comes from the day to day operation of running the company. This includes manufacturing, sales, and services provided.

Investing Cash Flow is where a company makes an investment. This would typically be purchasing equipment, property, and a building all that will affect the Fixed Assets on the Balance Sheet. And finally,

Financing Cash Flow is where a company acquires cash through financing. This is typically through loans, short and long term, issuing stock to inject cash into the business, and paying out dividends to stockholders.

To determine the cash flow, the Balance Sheet is used primarily to measure the changes in the amount of each account in Assets, Liabilities and Equity. As stated earlier, this is done monthly, quarterly or annually. An increase in Assets such as Inventory is a negative cash flow as growing inventory costs the company money. An increase in a Liability is a positive cash flow such as a new loan that will bring money into the company. And an increase in Equity will also be positive cash flow.

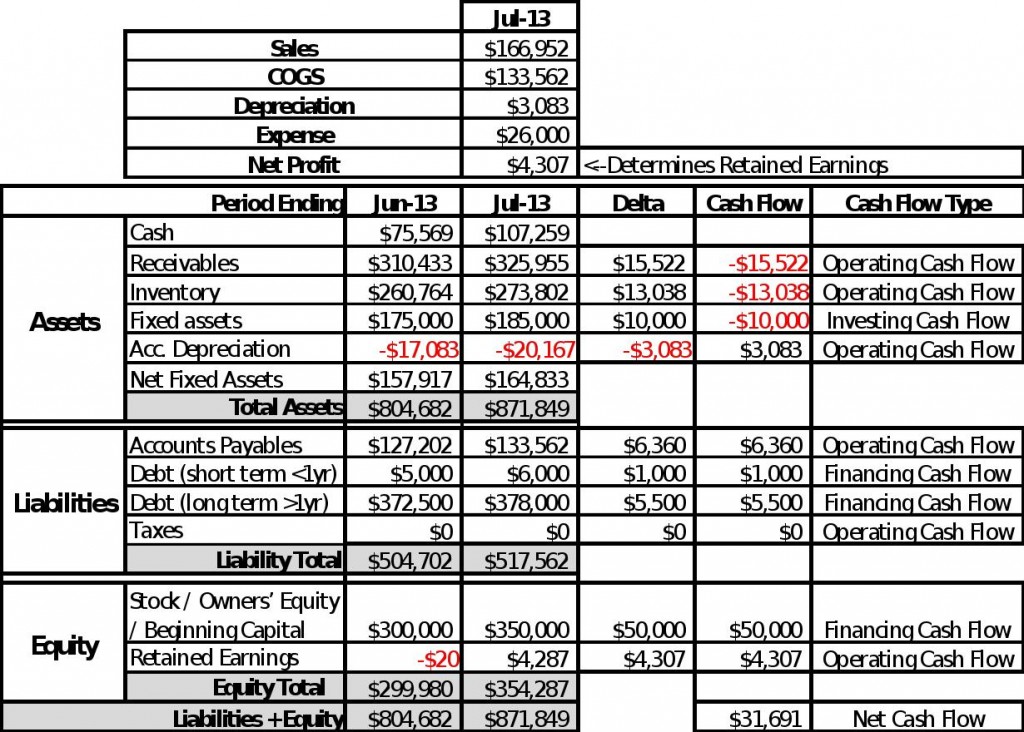

To do the math, I have used the financial statements from the prior two articles about the Income Statement and Balance Sheet.

The Delta column is the difference in the account for July minus June. Positive means the account grew, negative the account reduced. The Cash Flow column adjusts the delta column to whether that account is a positive (Liabilities and Equity) or negative (Assets) Cash Flow then adds them up to get the total net cash flow. That net cash flow determines the Cash Account by simple addition to the last money cash level.

Cash Jun-13 [$75,569] + net cash flow [$31.691] = Cash Jul-13 [$107,259]

As can be seen from this example, a positive Net Cash Flow increases the cash level in the cash account for the Balance Sheet of the company.

This completes the basic understanding of Financial Statements. Additional articles will be written on important metrics that can be found in these Financial Statements. The metrics will tell a company how it is performing financially as well as identify strengths and weaknesses so the company can take action to improve.

Here is some good news: FinancialSoft ‘s financial reporting system makes understanding financial statements easy. The reports are automatically calculated from your QuickBooks files and transposed into an easy to understand format the identifies the opportunities to improve cash flow in your company. Visit www.FinancialSoft.biz for more information

Recent Comments